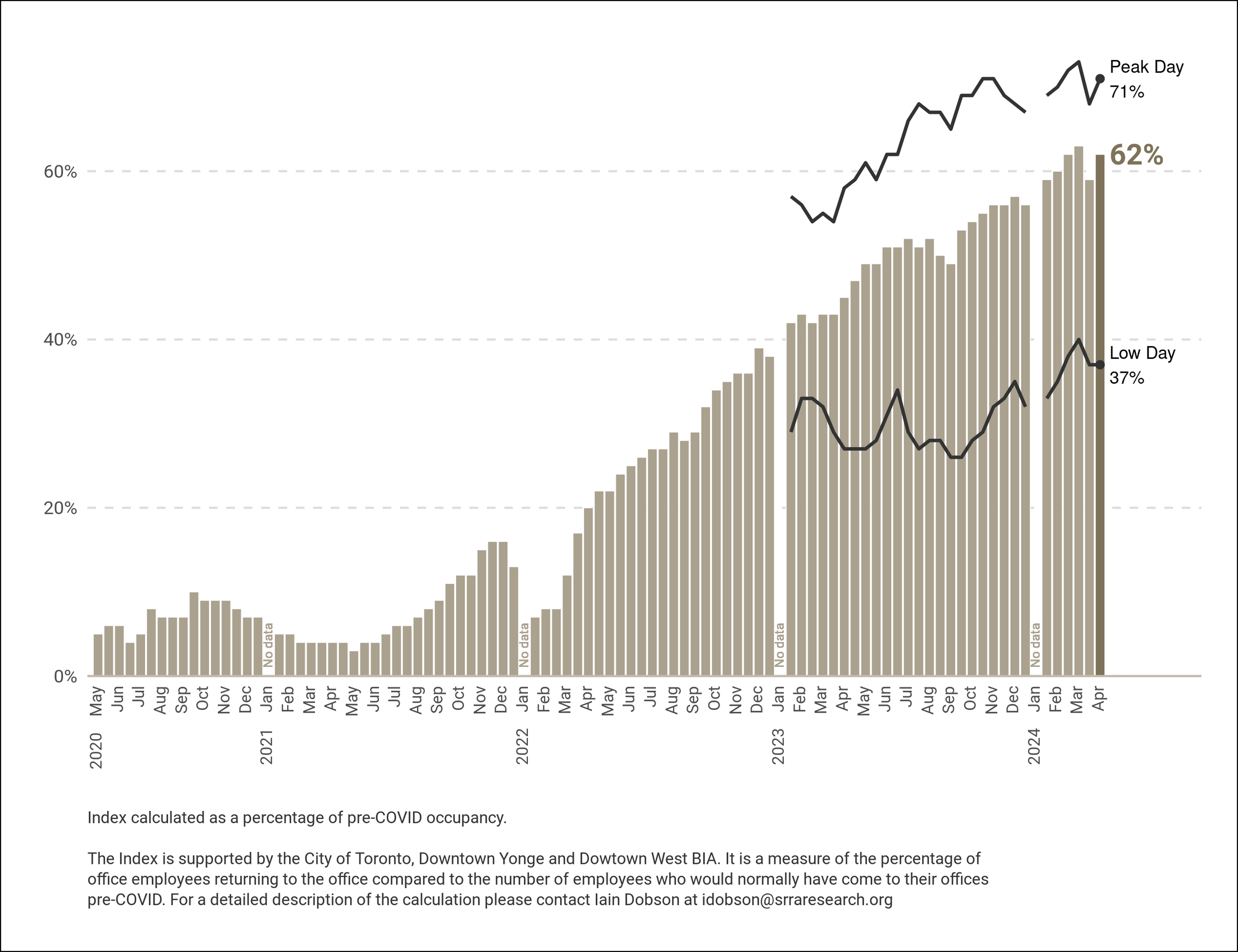

Average weekly - 62%

Peak Day - Wednesday 71%

Low Day - Friday 37%

The last week in March saw renewed activity downtown reflected in this month’s Index; we expect that to continue in April.

Our anniversary series of commentaries continues. Last week we prepared commentary on who is coming back to the office. The third of these commentaries addresses mobility challenges and the impact of COVID on congestion. We hope these expand commentaries will be useful for you.

Congestion is unacceptably high in all parts of the region and getting worse. At critical times of the day, roads are almost impassable, and transit is operating well below capacity. Travel patterns have changed. Remote work may appear to be allowing for less congestion in transit but certainly not on roads. Solving extreme congestion is now even more complicated because people’s workday travel plans are less predictable.

At the outset of the pandemic those who choose to travel abandoned public transit and resorted to a higher use of the automobile. This worked well when the Index was below 25% but as the return to the office everywhere in the region accelerated through the summer of 2023 the roads began to approach unacceptable levels not found since before the 2020 lockdown. In the downtown core of the city there is a finite inventory of parking spaces which, in theory, should keep congestion down. Try to explain that to drivers taking an hour to travel 2 kilometers. In the suburban areas of the region there is very little if any transit network connectivity to provide relief to highway congestion.

Is the answer to divert the movement of goods and service to low peak use of roads or create opportunities for centres where delivery companies can drop off and redistribute goods more efficiently and conveniently in highly dense areas?

Construction restrictions on road use, signaling enhancements, ramp access, and other traffic solutions are being explored throughout the region. In some cases, municipalities are making great strides. But the impact of these improvements is minimal.

Experts from many cities agree: roads have a finite capacity and when density in cities increases, roads have limits. The simple answer to congestion is for travellers to use other modes of travel than the car. Sounds easy enough.

Remote work may ease congestion on transit and to a lesser degree on roads, but remote work at the levels we see in the Index will not have the same impact as efficient and robust public transit networks. Remote work has not been cited in most studies because the impact on where and how people travel has yet to become apparent. The landscape keeps changing.

Toronto is experiencing population and employment growth at unprecedented levels. This presents challenges and opportunities. Improvements in road management are always welcome and that will help but unless there are convenient and accessible alternatives things won’t get better. The major challenge is to transit operators, starved for both ridership and operating revenue, is keeping pace with growth.

The simple fact of the matter is we need to support transit operators and find ways to increase transit use. Remote work won’t have much of a real impact on the continued intensification of this city and the region, but population growth will.

Your SRRA team

Links to Articles of Interest

Shifting Travel Patterns in Downtown Vancouver Keeping Restaurants in the Red

Although Vancouverites have rediscovered downtown post-pandemic they are visiting less often and spending less in response to rising food prices, a new report by the U of T’s School for Cities has found. The report, which compares recovery rates among hundreds of downtowns across North America, places Vancouver ahead of Toronto, citing the benefits of a large resident population downtown. Restaurants and entertainment venues remain the hardest hit.

Foot Traffic Higher in Pricier Digs? Amenity-Rich Offices Generate More In-Office Activity

Although not a scientific assessment, a report from New York that looked at 25 buildings with highest rents suggests that employers’ expectations for investing in the quality of office space pay off in terms of workers showing up in-office.

Office Utilization Across U.S. Federal Government Barely in Double Digits

A new report from the Public Buildings Reform Board suggests that government leaders are not pushing employees to return to their offices. Some buildings in Washington D.C. have 12% occupancy.

Manhattan Landlords Struggling as Employers Reduce Office Footprint

Availability is uncomfortably high suggest some landlords, although the numbers cited include older, less competitive buildings.

WeWork Close to Emerging from Bankruptcy – Puts a Brave Face on Its Future

By significantly reducing the number of locations across the world from 500 to 300 plus or minus, WeWork expects to be ready for a more positive future, reports suggest.

“The Occupancy Index is supported by the City of Toronto, Downtown Yonge BIA, and Downtown West BIA. It is a measure of the percentage of office employees returning to the office compared to the number of employees who would normally have come to their offices pre-COVID. For a detailed description of the calculation please contact Iain Dobson at [email protected],”